Struggling with Homeowner’s Insurance?

Revelations From the California Insurance Commissioner’s Marathon Virtual Hearing

The good news from the pandemic: the state has learned how to do Zoom. We no longer have to trek to Sacramento to work with state officials; we can now do it from our living rooms. Direct democracy in action!

We met Insurance Commissioner Ricardo Lara last year when Assembly Member Monique Limón brought him here to meet with us because we were starting to experience the newly emerging statewide problem of non-renewals tied to high wildfire risk. Fast forward to today – after 4.1 million acres just burned.

Insurance Commissioner Lara scheduled a mega virtual hearing with homeowners, fire chiefs, consumer advocacy groups, and insurers on the problems of non-renewal, under-insurance, Fair Plan, and climate change mitigations. Here are the highlights:

1. Several fire chiefs spoke, including our own Chief Kevin Taylor, who did a great job! The message was pretty consistent: we’re fire-proofing around here. We have a Fire Safe Council, a Community Wildfire Protection Plan (Montecito was the first to file one in Santa Barbara County). There are sheep eating brush off the mountain, wood-chipping and brush-clearing activities. Homeowners are hardening their homes and creating defensible spaces.

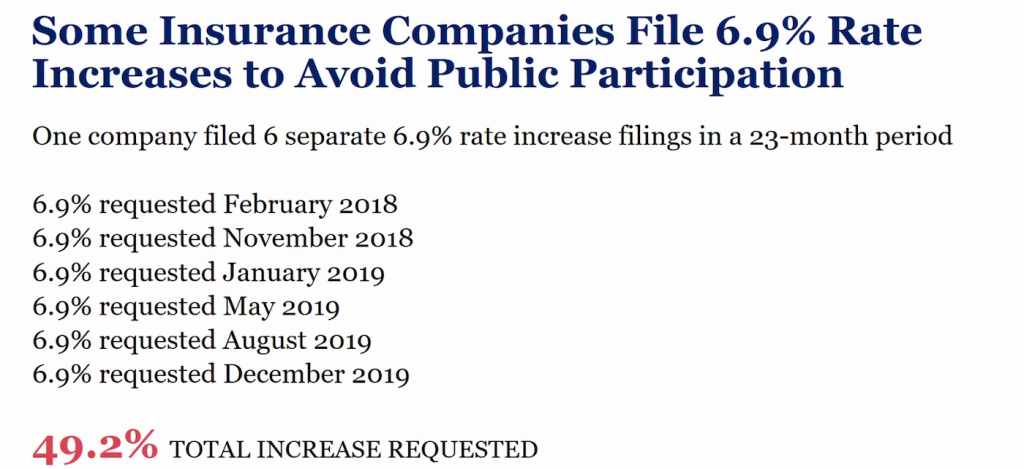

2. Prop 103 regulates insurance company rate increases.They can file rate increases of up to 7 percent with no public hearings. Above 7 percent, it triggers public review, which are called “interventions.” Members of the public can push back against the rate increase, and extend the time for approval. To avoid interventions, many insurers game the process.

Homeowners who live in a fire risk area willpay higher premiums. A rate filing for a request of 6.9 percent could result in 30 percent reduction for one home in a zero fire risk area, and an 80 percent increase for a homeowner in high fire risk area.

3. Several insurers presented their case. They wanted easier paths to rate increases. Denied those, and facing higher risks in wildfire areas, they largely decided to abandon writing policies in those areas. If the insurance companies can’t increase premiums outside the Prop 103 process that triggers public review, according to State Farm, the largest carrier in the state, to the level needed to cover risk, they can’t succeed. Every week’s delay in a rate increase request of 6.9 percent equals $1.6 million they aren’t getting in premiums to cover claims filed.

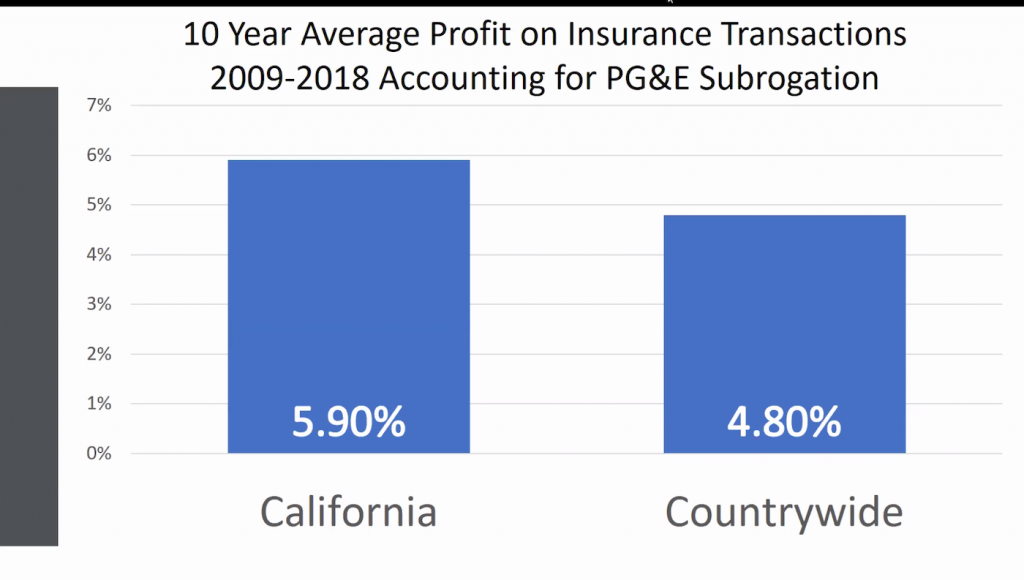

California is a very profitable market, especially with the $11 billion PG&E settlement.

4. Several advocacy groups weighed in on climate change, calling for different risk models that reflect the world we’ve known in the past three years, rather than the past 20. In 2016, some consumer groups said wildfire rates were going down, so premiums should drop. We know how that turned out. Insurance companies were pushed to use better replacement cost estimator tools, widely known to lowball the actual cost of replacement items, and leave you underinsured, while you believed you were fully insured. I asked, as did other communities, on what about climate change mitigation? What about communities that underground utilities, reduce their community-wide risk of fire, harden their infrastructure – is any of this going to matter in insurance companies’ calculations when they don’t send assessors in to evaluate those mitigations? The insurers maintain their costs are regulated by the California Department of Insurance and don’t allow for assessments of mitigation strategies. Local land use codes need updating for building / rebuilding in the WUI to force mitigations on homeowners.

5. All of this has driven many desperate homeowners to the California Fair Plan, which has plenty of its own problems, including refusing to underwrite some homes, underinsuring others, and not having large enough limits to cover many properties. Here is the effect of non-renewals from voluntary insurers on the uptake of the Fair Plan.

Closing Statements

Commissioner Lara said he appreciated that homeowners and communities had done so much work to harden against ember spread. But the sacrifice should not all be on the homeowners’ side. We need greater partnership with our insurers. Today we’ve seen evidence insurers game the system to fly under the radar of public scrutiny. If the insurance industry wants higher rates, they need to maintain the solvency of the industry. We need insurers to stop cherry-picking some homeowners while abandoning others. Home ownership serves as a primary source of wealth accumulation in California. Not being able to get affordable insurance, and not being able to access resources to harden your community can lead to a downward spiral in our state’s housing market. When people have taken steps to harden their homes and communities, it should be taken into account in premiums. It’s time to show our resolve and commitment to these protective measures, and for insurance carriers to work with us. We know there are updated models that can take recent events into account to better assess risk, and we want to pursue incorporating those that are proven. We also want local land use authorities to update their codes to push risk mitigation strategies.