Most of Montecito Not a “High Risk” Zone

GUEST EDITORIAL

by Harry McMullan

(Mr. McMullan wrote the following to the Santa Barbara Fire chief, Santa Barbara County sheriff, and all five County supervisors.)

My wife and I are residents of Montecito, and we appreciate beyond words the inspiring work of all the firefighters and other first responders who so selflessly and brilliantly saved all but a few homes in our community in the Thomas Fire.

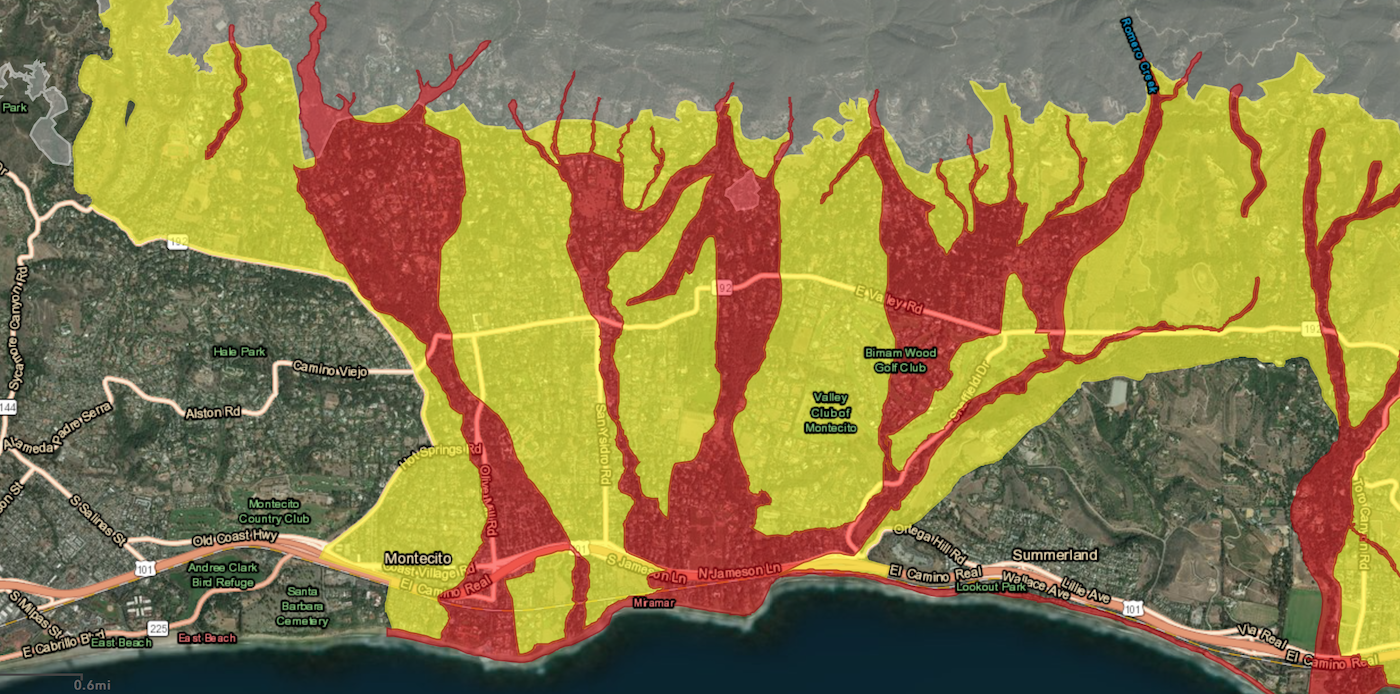

On the Debris Flow Risk Area map released recently, our home, like most of the homes in Montecito, is located in what has been designated a “High Risk” yellow zone. That “High Risk” nomenclature is seriously faulty, because the designations for the “Extreme Risk” red zone and the “High Risk” zone imply only a different degree of the same type of risk between the two zones. In fact, the “yellow” zones represent a wholly different type of risk presented by the “red” zones.

At the public meeting, we learned how the Debris Flow Risk Area map was constructed, and I take for granted that the delineation of the respective areas represents the best forecast by experts of possible future debris flow (red) zones, as well as those (yellow) zones in which the inhabitants might be temporarily cut off without electricity, water, gas, phone service, or sewer.

Thus in the red zones, people’s lives and homes are at “Extreme Risk” from debris flows, whereas in the yellow “High Risk” zones, the jeopardy is limited to being “cut off” for some days, but – and here is the critical distinction for insurance companies and mortgage lenders – risk of damage to homes from debris flows is not suggested. In other words, in the yellow zone, case mortgage lenders may expect to retain their collateral: a decisive factor for them.

Here is how the two zones are described on the Debris Flow Risk Area map:

Red Zones:

Extreme Risk – Your property is located in an extreme risk area. This means that debris flows similar to the 1/9 debris flow could impact you. If rain is predicted to be a half-inch per hour or more, you would be ordered to evacuate. You should leave immediately and seek shelter in a location outside the evacuation area.

Yellow Zones:

High Risk– Your property is located in a high-risk area. If rain is predicted to be a half-inch per hour or more, you would be at risk from being cut off from essential services such as natural gas, potable water, sewer, electricity, cellular phone service, and other utilities for multiple days. Roads may become impassable and even deadly. You should leave immediately and seek shelter in a location outside the evacuation area.

Change the Designation

Our hearts go out to those whose homes are in the red “Extreme Risk” zones for many reasons, not the least of which is that even if their 1/9 losses are covered by their insurance companies, it’s far-fetched to imagine any non-governmental insurance company again offering insurance on homes in that zone – other than perhaps at punitive cost. Without insurance, no mortgages will be issued, and without the ability of owners to get mortgages, it’s difficult to imagine many new houses being built in the red zones.

This situation entails disastrous consequences not only for the hundreds of red zone property owners and for the community as a whole, but also for the tax base of the county, already faced with daunting emergency, repair, and restoration costs.

I suggest that we need a more accurate descriptor for the yellow zone, one that makes it clear to insurance and mortgage companies that properties in the yellow zones are not merely at a somewhat lower risk of being swept away than the red zone properties than the labels “Extreme Risk” and “High Risk” imply.

Insurance companies lump policies in different groups before selling them to reinsurers, and the present terminology of “Extreme Risk” and “High Risk” fails to make a meaningful risk distinction between those two groups immediately apparent to a reinsurance executive sitting at his desk in Zurich. Absent such a distinction, the yellow zone properties in Montecito – which accounts for most of them – might be lumped into a category that, in turn, could make finding affordable insurance coverage much more difficult for the entire community.

The risk to the red zone areas isn’t going away with any change of definition. However, the current yellow zone “High Risk” properties are not subject to any noted risk of being swept away by a debris flow, as the stand-alone title might lead a far-removed insurance or mortgage company executive to suppose. Instead of “High Risk,” the yellow zone could be renamed a “High Risk of Temporary Exclusion” zone or at least something that accurately reflects the intent of the accompanying definition. [Editor’s note: We prefer “Likely Risk of Temporary Service Interruption.”]

I believe that such a change of wording might be helpful in preventing huge hikes in insurance policy costs for yellow zone residences, which would help facilitate a quicker recovery for the local real estate market, on which so much depends for the welfare of homeowners, not to mention the tax base of the County of Santa Barbara.

You might also be interested in...